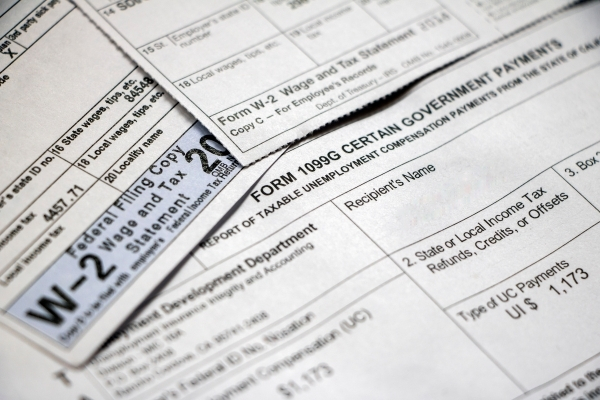

W-2 vs. 1099: Which workers get which?

As the gig economy continues to expand, employers now more than ever need to possess a thorough understanding of the classification for each person performing services for the company. Knowing whether the IRS views someone as your employee or as an independent contractor dictates tax obligations and associated paperwork, namely whether you bear responsibility for filing a W-2 or a 1099 for the individual in question.

As the gig economy continues to expand, employers now more than ever need to possess a thorough understanding of the classification for each person performing services for the company. Knowing whether the IRS views someone as your employee or as an independent contractor dictates tax obligations and associated paperwork, namely whether you bear responsibility for filing a W-2 or a 1099 for the individual in question.

Don’t risk getting in trouble by issuing the wrong form. Take a closer look at what W-2s and 1099s entail.

W-2

W-2: Wage and Tax Statement is a critical, annual document that reports an employee’s gross earnings for the entire year. It also states the cumulative amount of taxes the employer withheld each time the business issued the individual a paycheck.

Expect that virtually every employee will require a W-2. By law, an employer must fill out a W-2: Wage and Tax Statement for each of its employees to whom it paid $600 or more for the year or for whom it withheld any taxes.

Several different parties need the information contained in a W-2, which is why the form exists as a six-copy packet. The Social Security Administration (SSA) receives Copy A. The state, city, or local tax department gets Copy 1. Copies B, C, and 2 go to the employee. Employers retain Copy D in their records for a period of four years.

The law requires employers to file W-2s with the SSA by January 31 of the year following the year in which the wages were paid. Likewise, appropriate copies must be given to or mailed to employees on or before this due date. If the 31st falls on a Saturday, Sunday, or legal holiday, the due date gets pushed to the next business day.

An accurate W-2 is important to employees. They need the information it contains to complete their own individual tax return. Also, future social security and Medicare benefits are computed based on these figures.

1099

Similarly, the IRS requires organizations to report information about people who perform work for the company but are not on the payroll. This involves filling out Form 1099-NEC: Nonemployee Compensation.

(Note: Do not use Form 1099-MISC for this purpose. While this form used to be the appropriate one for reporting nonemployee compensation, the IRS switched to 1099-NEC beginning with tax year 2020.)

Unlike the case for employees, employers generally do not have to withhold or pay any taxes on payments to independent contractors. These individuals keep track of their own tax obligations, oftentimes making quarterly estimated tax payments to the government. They fill out appropriate forms dealing with their earnings as part of their annual personal tax return.

While smart independent contractors meticulously keep their own records as to who paid them what, the law still requires official reporting. Thus, an employer must file a 1099-NEC for each person who is not an employee but to whom it paid at least $600 during the course of a year for services performed.

Like a W-2, a 1099-NEC contains multiple copies that go to different places. Copy A goes to the IRS, and Copy 1 goes to the state tax agency. The independent contractor receives Copy B and Copy 2. The employer keeps Copy C in its records. Also like a W-2, the 1099-NEC has a due date of January 31.

Why and how to determine worker classification

The work done by employees and independent contractors often looks the same. For instance, a company may maintain an editorial staff that writes its PR releases and oversees its blog. It also may bring aboard freelancers to lend expertise on a certain subject or handle overflow assignments.

Though performing similar actions, the law views these two employment relationships in different ways. Assigning the label “employee” or “nonemployee” determines actions such as:

- Whether or not the employer assumes responsibility for withholding federal, state, social security, and Medicare taxes.

- Whether the employer must issue a W-2 or a 1099-NEC.

- Whether or not certain federal and state labor and employment laws apply.

- How and when someone gets paid (hourly or salary on a set basis for an employee vs. under the terms of an agreed-upon “statement of work” for an independent contractor).

The IRS offers guidelines for classifying someone as an employee or as an independent contractor. In general, greater control and independence by the worker himself points toward classification as an independent contractor. Issues examined often include:

- Does the company or the worker control how, when, and where work gets performed?

- Does the company provide tools and supplies or is that the worker’s responsibility?

- Does the company offer the person benefits that typically signify an on-going relationship, such as a retirement plan, health insurance, and paid vacation?

- Is the worker subjected to annual reviews or other evaluation systems commonly used to offer feedback to permanent staff and determine raises and promotions?

- Does the employer regularly require the worker to update skills or attend trainings to better meet company needs?

- Does the worker expect to receive a regular paycheck, or does he sign an agreement to receive a set sum of money in exchange for performing certain tasks?

- Do both employer and worker see the relationship as permanent or as subject to end once terms of an agreed-upon contract are complete?

Still unsure whether to consider someone an employee or an independent contractor because different factors point in different directions? Employers truly uncomfortable making the distinction themselves can file Form SS-8, Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding. The IRS will review the facts and circumstances to officially determine the worker’s status. Unfortunately, such a judgment can take around six months to receive. For businesses that continually hire the same types of workers to perform particular services, though, receiving an official “final decision” may be worth the effort and wait.