When are 1099s due? 1099-NEC, 1099-MISC, and additional forms

Avoiding penalties: Meeting IRS 1099 deadlines

Not all businesses will need to file 1099 forms. However, for those that do, it’s important to meet the IRS deadlines, whether paper filing or e-filing. Not doing so, and not filing for extensions, will land you with fines and draw unwanted attention.

The due date for 1099s will vary based on the particular form you need to use, as well as how you file. The Internal Revenue Service has set different dates, for many forms, based on whether you use traditional paper or electronic filing.

So let’s take a look at what forms you may need to file, and when the due dates are for tax year 2022. As a reminder, forms for the previous tax year are due in the following calendar year, so the following dates will fall in 2023.

What are 1099s used for?

As a reminder, 1099 forms are used for nonemployee compensation. For most businesses, this will apply to freelancers, independent contractors, and others who do work for you, but are not primarily employed by you. Compensation paid to your employees is handled on forms w-2.

There are some additional 1099 forms that have specific uses that we’ll take a look at later.

Common 1099 forms and due dates

First, we’ll look at the most common 1099 forms you may see.

Form 1099-NEC

Form 1099-NEC was a new form released to use in place of Form 1099-MISC for nonemployee compensation. It is used to report payments of at least $600 to freelancers and independent contractors.

This form is due to both the IRS and Recipient by January 31st.

Form 1099-MISC

1099-MISC: Miscellaneous Information (sometimes referred to as miscellaneous income), covers a wide variety of types of compensation.

Some of its more common uses are:

-

Prizes and awards.

-

Payments made to health and medical service suppliers through medical assistance programs or insurance plans.

-

Substitute dividends and tax-exempt interest payments reportable by brokers.

-

Payments to attorneys.

-

Finishing boat crew payments and proceeds.

In most cases, this form is due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st, except when being used for attorney feeds or substitute dividends and tax-exempt interest payments. In that case, it is not due to the recipient until February 15th.

Other 1099 form filing deadlines

While most follow the same deadlines as 1099-MISC, there are some variations in due dates. Below we’ve listed each form and when it’s due to the IRS as well as the recipient, along with any variations in due date if you choose to e-file.

-

1099-A. Acquisition or Abandonment of Secured Property. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients (borrowers) by January 31st.

-

1099-B. Proceeds From Broker and Barter Exchange Transactions. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by February 15th, or March 15th for reporting by trustees and middlemen of WHFITs.

-

1099-C. Cancellation of Debt. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st.

-

1099-CAP. Changes in Corporate Control and Capital Structure. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to shareholders by January 31st and to clearing organization by January 5th.

-

1099-DIV. Dividents and Distributions. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st, or March 15th for reporting by trustees and middlemen of WHFITs.

-

1099-G. Certain Government Payments. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st.

-

1099-H. Health Coverage Tax Credit (HCTC) Advance Payments. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st.

-

1099-INT. Interest Income. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st, or March 15th for reporting by trustees and middlemen of WHFITs.

-

1099-K. Payment Card and Third Party Network Transactions. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st.

-

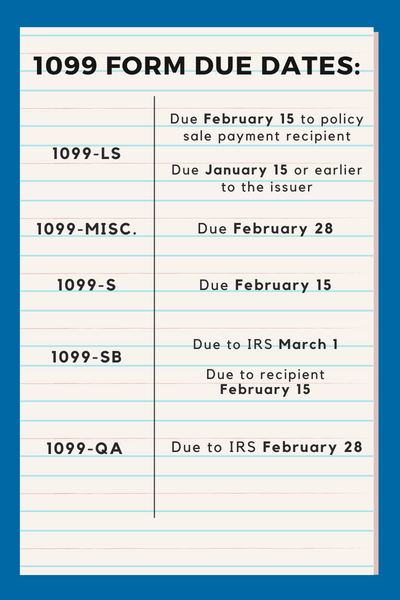

1099-LS. Reportable Life Insurance Sale. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. For reportable policy sale payment recipient, February 15; For issuer, January 15, or earlier as required by Regulations section 1.6050Y-2(d) (2)(i)(A)

-

1099-LTC. Long-Term Care and Accelerated Death Benefits. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st.

-

1099-OID. Original Issue Discount. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st, or March 15th for reporting by trustees and middlemen of WHFITs.

-

1099-PATR. Taxable Distributions Received From Cooperatives. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st.

-

1099-Q. Payments From Qualified Education Programs (Under Sections 529 and 530). Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st.

-

1099-QA. Distributions From ABLE Accounts. Due to the IRS by February 28th. It is due to recipients by January 31st.

-

1099-R. Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st.

-

1099-S. Proceeds from real estate transactions. Due to the recipient Feb 15.

-

1099-SA. Distributions From an HSA, Archer MSA, or Medicare Advantage MSA. Due to the IRS by February 28th if filed by paper, and March 31st if e-filed. It is due to recipients by January 31st.

-

1099-SB. Seller’s Investment in Life Insurance Contract. Due to the IRS March 1st if filed by paper, and March 31st if e-filed. Due to the recipient February 15.

Additional considerations

Weekends and holidays

If any tax form deadline falls on a Saturday or Sunday, or on a legal holiday in the state the form is to be filed, it will be due the next business day. Looking at the calendar for 2023, it does not appear like any form deadlines fall outside of normal business days.

30 day extension

If you do not believe you will make the deadline, you can file Form 8809 Application for Extension of Time to File Information Returns with the IRS. With this form, you can request to extend the deadline, however, there are limited circumstances in which you’ll be permitted to do so.

You only qualify for an extension if:

-

The filer suffered a catastrophic event in a federally declared disaster area that made the filer unable to resume operations or made necessary records unavailable.

-

Fire, casualty, or natural disaster affected the operation of the filer.

-

Death, serious illness, or unavoidable absence of the individual responsible for filing the information returns affected the operation of the filer.

-

The filer was in the for establishment.

-

The filer did not receive data on a payee statement such as Schedule K-1, Form 1042-S, or the statement of sick pay required under section 31.6051-3(a)(1) in time to prepare an accurate information return.

If you still have an ongoing issue near the end of your 30 day extension, it may be possible to file additional extensions. In most cases, you may also file your extension online at https://fire.irs.gov/. However, you cannot use the online system when requesting an extension for Forms 1099-NEC or 1099-QA.

Finally, if you wish to file for an extension, it must be done before the due date of the form. It cannot be done after a deadline has already been missed.

File 1099s correctly and on time to avoid penalties

You’ll want to get your 1099 forms submitted correctly and by the due date as you may be subject to a penalty for failing to do so. If you do not make the deadline, you may still complete a late filing, however, you will be subject to penalties based on the filing date.

Penalties may apply:

-

If you fail to file timely.

-

If you fail to include all information required to be shown on a return.

-

If you include incorrect information on a return.

-

If you file on paper when you were required to file electronically.

-

If you report an incorrect TIN.

-

If you fail to report a TIN.

-

If you fail to file paper forms that are not machine-readable and applicable revenue procedures provides for a machine-readable paper form.

Penalties increase the longer you wait to correct them

If you realize you made a mistake, it’s important to address it as quickly as possible to avoid paying increased fees.

The penalty is as follows:

-

$50 per information return if you correctly file within 30 days (by March 30 if the due date is February 28); maximum penalty $565,000 per year ($197,500 for small businesses, defined below).

-

$110 per information return if you correctly file more than 30 days after the due date but by August 1; maximum penalty $1,696,000 per year ($565,000 for small businesses).

-

$280 per information return if you file after August 1 or you do not file required information returns; maximum penalty $3,392,000 per year ($1,130,500 for small businesses).

What to do if you make a mistake

Fortunately, correcting a mistake isn’t too difficult – but you want to do it quickly. There are two types of errors – each with slightly different steps to address them.

Error Type 1 – This is if your mistake involved an incorrect amount of money, code, or checkbox. To correct it, follow these simple steps:

-

Prepare a new information return.

-

Enter an “X” in the “CORRECTED” box at the top of the form.

-

Correct any recipient information and report other information as per the original return.

-

Error Type 2 – These mistakes are a little more complicated to fix – and include the following mistakes; no payee TIN, incorrect payee TIN, or incorrect payee name. To correct this, follow these steps:

Step 1:

-

Prepare a new information return.

-

Enter an “X” in the “CORRECTED” box at the top of the form.

-

Enter the payer, recipient, and account number information exactly as it appeared on the original incorrect return; however, enter -0- (zero) for all money amounts.

-

Step 2:

-

Prepare a new information return.

-

Do not enter an “X” in the “CORRECTED” box at the top of the form. Prepare the new return as though it is an original.

-

Include all the correct information on the form including the correct TIN and name.

-

A few time-saving tips

TIN matching

The easiest way to stave off penalties for name/Taxpayer Identification Number (TIN) mismatches is to use the IRS’ online TIN matching program before completing 1099-MISC/1099-NEC forms. You may verify up to 25 name/TIN combos on the screen. However, you must register with the IRS to use this program.

Additional Resource: Learn more about TIN matching from the IRS.

TIN truncation

You may truncate the first five digits of a payee’s TIN on their paper or electronic copies; forms filed with the IRS must contain the full TIN. These TTINs, as they’re called, look like this: XXX-XX-1234 or ***-**-1234 for SSNs, or XX-XXX1234 or –*1234 for EINs. You can’t truncate your own EIN.

More resources:

Digital age workplace: Why soft skills matter more than ever

Talent shortage: Addressing the growing gap in the workplace

Employee skill gaps: What they are and how to address them